2018? Expect more volatility!

Despite the usual worry list, 2017 has been pretty good for investors as global growth and profits accelerated and central banks stayed benign as inflation stayed low.

2017 – a relatively smooth year

By the standards of recent years, 2017 was relatively quiet. Sure there was the usual “worry list” – about Trump, elections in Europe, China as always, North Korea and the perennial property crash in Australia. And there was a mania in bitcoin. But overall it has been pretty positive for investors:

- Global growth continued the acceleration we had seen through the second half of last year. In fact, global growth looks to have been around 3.6%, its best result in six years, with most major regions seeing good growth. Solid global growth helped drive strong growth in profits.

- Benign inflation. While deflation fears faded further, underlying inflation stayed low and below target, surprising on the downside in the US, Europe, Japan and Australia.

- Rising commodity prices. Better than feared global demand and a surprise fall in the $US helped commodity prices along with constrained supply in the case of oil.

- Politics turned out to be benign. Political risks featured heavily in 2017 but they turned out less threatening than feared: while political risk around Trump rose with the Mueller inquiry into his presidential campaign’s Russian links, business-friendly pragmatism dominated Trump’s first-year policy agenda and a trade war with China did not eventuate; Eurozone elections saw pro-Euro centrists dominate; North Korean risks increased but didn’t have a lasting impact on markets; Australian politics remained messy but arguably no more so than since 2010.

- Another year of easy money. While the Fed continued to gradually raise interest rates and started reversing quantitative easing and China tapped the monetary brakes, central banks in Europe and Japan remained in stimulus mode and overall global monetary policy remained easy.

- Australia had okay growth hitting 26 years without a recession, but inflation remained below target. While housing construction started to slow and consumer spending was constrained, non-mining investment improved, infrastructure spending surged & export volumes were strong. Record low wages growth and low inflation kept the Reserve Bank of Australia (RBA) on hold, though.

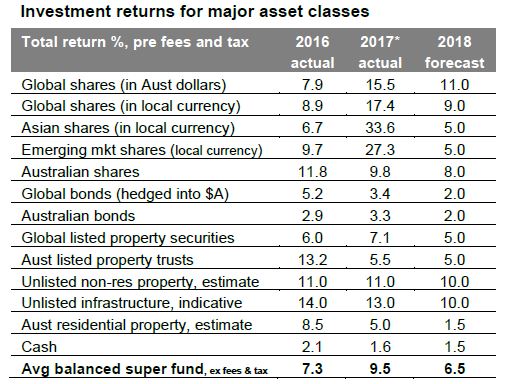

The “sweet spot” of solid global growth and low inflation/benign central banks helped drive strong investment returns overall.

Yr to date to Nov. Source: Thomson Reuters, Morningstar, REIA, AMP Capital

- Global shares pushed sharply higher supported by strong earnings, low interest rates and growing investor confidence. While Eurozone, Japanese and Australian shares saw 5-7% corrections along the way, US shares only saw brief 2-3% pullbacks. So volatility was very low.

- The big surprise was that the US dollar fell rather than rose as low inflation kept expectations for Fed rate hikes depressed. This helped boost US shares but dragged on Eurozone shares as the Euro rose.

- Asian and emerging market shares were star performers thanks to leverage to global growth, rising commodity prices and a weaker $US, which reduced debt servicing costs.

- Australian shares had good returns but were relative laggards as has generally been the case this decade with weaker underlying profit growth.

- Bonds had mediocre returns. While inflation surprised on the downside, ultra-low yields constrained returns.

- Real estate investment trusts had a somewhat constrained year as investors remained a bit wary of listed yield plays.

- Unlisted commercial property and infrastructure continued to do well as investors sought their still relatively high yields.

- Australian residential property returns slowed as the heat came out of the Sydney and Melbourne property markets.

- Cash and bank term deposit returns were poor reflecting record low RBA interest rates.

- Reflecting US dollar softness, the $A actually rose helped by modest gains in commodity prices.

- Reflecting strong returns from shares and unlisted assets, balanced superannuation fund returns were strong.

2018 – looking ok but expect more volatility

2018 is likely to remain favourable for investors, but more constrained and volatile. The key global themes are likely to be:

- Global growth to remain strong. Global growth is likely to move up to 3.7%, ranging from around 2% in advanced countries to around 6.5% in China, with the US receiving a boost from tax cuts. Leading growth indicators such as business conditions PMIs point to continuing strong growth, but just bear in mind that they don’t get much better than this. Overall, this should mean continuing strong global profit growth albeit momentum is likely to peak.

Source: Bloomberg, IMF, AMP Capital

- US inflation starting to lift. Global inflation is likely to remain low, but it’s likely to pick up in the US as spare capacity is declining, wages growth is picking up and as higher commodity prices feed through. We don’t expect a surge and the flow through in other major countries will be gradual. But higher US inflation may disrupt the yield trade at times and cause some nervousness.

- Monetary policy divergence to continue. The Fed is likely to hike four times in 2018 (which is more than markets are allowing) and to continue with quantitative tightening but other central banks are likely to lag.

- Political risk may have more impact after a relatively benign 2017. US political risk is likely to become more of a focus again (with the Mueller inquiry getting closer to Trump, the November mid-term elections likely to see the Republicans lose the House and the risk that Trump may resort to populist policies like protectionism to shore up his support), the Italian election is likely to see the anti-Euro Five Star Movement do well (albeit not well enough to form government), North Korean risks are unresolved and there is the risk of an early election in Australia. Fortunately, there is still no sign of the sort of excesses that drive recessions and deep bear markets in shares: there has been no major global bubble in real estate or business investment; there is the bitcoin mania but not enough people are exposed to that to make it economically significant globally; inflation is unlikely to rise so far that it causes a major problem; share markets are not unambiguously overvalued and global monetary conditions are easy. So arguably the “sweet spot” remains in place, but it may start to become a bit messier. For Australia, while the boost to growth from housing will start to slow and consumer spending will be constrained, a declining drag from mining investment and strength in non-mining investment, public infrastructure investment and export volumes should see growth around 3%. However, as a result of uncertainties around consumer spending along with low wages growth and inflation, the RBA is unlikely to start raising interest rates until late 2018 at the earliest.

Implications for investors

Continuing strong economic and earnings growth and still-low inflation should keep overall investment returns favourable but stirring US inflation, the drip feed of Fed rate hikes and a possible increase in political risk are likely to constrain returns and increase volatility after the relative calm of 2017:

- Global shares are due a decent correction and are likely to see more volatility, but they are likely to trend higher and we favour Europe (which remains very cheap) and Japan over the US, which is likely to be constrained by tighter monetary policy and a rising US dollar. Favour global banks and industrials over tech stocks that have had a huge run.

- Emerging markets are likely to underperform if the $US rises as we expect.

- Australian shares are likely to do okay but with returns constrained to around 8% with moderate earnings growth. Expect the ASX 200 to reach 6200 by end 2018.

- Commodity prices are likely to push higher in response to strong global growth.

- Low yields and capital losses from a gradual rise in bond yields are likely to see low returns from bonds.

- Commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield by investors.

- National capital city residential property price gains are expected to slow to around zero as the air comes out of the Sydney and Melbourne property boom and prices fall by around 5%, but Perth and Darwin bottom out, Adelaide and Brisbane see moderate gains and Hobart booms.

- Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.2%.

- The $A is likely to fall to around $US0.70, but with little change against the Yen and the Euro, as the gap between the Fed Funds rate and the RBA’s cash rate goes negative.

What to watch?

The main things to keep an eye on in 2018 are:

- The risks around Trump – the Mueller inquiry and the mid-term elections. We don’t see the Republicans impeaching Trump (unless there is evidence of clear illegality) but he could turn to more populist policies such as a trade war with China, a spat over the South China Sea or a clash with North Korea to boost his support.

- How quickly US inflation turns up – a rapid upswing is not our base case but it would see a more aggressive Fed, more upwards pressure on the $US, which would be negative for US and emerging market shares and a rapid rise in bond yields.

- The Italian election – the anti-Euro Five Star Movement is likely to do well and, even though it’s hard to see them being able to form government, this could cause nervousness;

- Whether China post the Party Congress embarks on a more reform-focussed agenda resulting in a sharp decline in economic growth – unlikely but it’s a risk.

- Whether non-mining investment, infrastructure spending and export volumes are able to offset constrained consumer spending and a downturn in the housing cycle and how far Sydney and Melbourne property prices fall.

Published with permission from AMP. For original source, disclaimers and credits please see: http://www.ampcapital.com.au/news/olivers-insights

Comments are closed.